Penn has adopted the Integrated Internal Control Framework (IICF), an adaptation of COSO (Committee of Sponsoring Organizations of the Treadway Commission), for utilization as the foundation of the internal control and compliance environment.

This Framework defines internal control is a process, effected by an entity’s board of directors, management and other personnel. This process is designed to provide reasonable assurance regarding the achievement of objectives in the following categories:

- Effectiveness and efficiency of operations.

- Reliability of financial reporting.

- Compliance with applicable laws and regulations.

This definition reflects certain fundamental concepts:

- Internal control is a process. It is a means to an end, not an end in itself.

- Internal control is effected by people. It is not merely policy manuals and forms, but people functioning at every level of an organization.

- Internal control is geared to the achievement of objectives in several overlapping categories.

- Internal control can be expected to provide only reasonable assurance, not absolute assurance, to the institution’s leaders regarding achievement of operational, financial reporting and compliance objectives.

Effective administration involves planning, executing and monitoring. Internal control is a tool used by administrators to accomplish these processes.

Management’s Responsibility For Internal Control

In accordance with University Policy 2701, management is responsible, in both the central and decentralized operating units, for establishing, maintaining and promoting effective business practices and effective internal controls. Such systems of internal control will vary from activity to activity depending upon the operating environment, including the size of the entity, its diversity of operations and the degree of centralization of financial and administrative management.

While there may be practical limitations to the implementation of some internal controls, each business function throughout the University and Penn Medicine must establish and maintain a system of controls which meets the minimum requirements as established by the University’s Internal Control Policy. A properly functioning system of controls improves the efficiency and effectiveness of operations, contributes to safeguarding assets and identifies and discourages irregularities, such as questionable or illegal payments and practices, conflict of interest activities and other diversions of assets.

Components of Internal Control

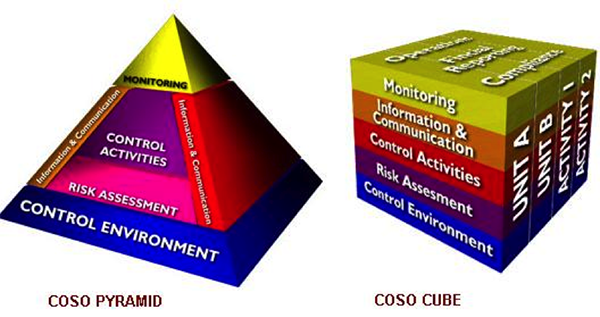

Internal Control consists of five interrelated components derived from basic University operations and administrative processes as follows:

- Control Environment – The core of any educational institution is its people. They are the engine that drives the organization. Their individual attributes (integrity, ethical values and competence) and the environment in which they operate determine the success of the institution.

- Risk Assessment – Colleges and universities must be aware of and deal with the risks they face. They must set objectives that integrate key activities so the total organization operates in concert. They also must establish mechanisms to identify, analyze, and manage the related risks.

- Control Activities – Control policies and procedures must be established and executed to help ensure that actions necessary to achieve the institution’s objectives are effectively carried out.

- Information and Communication – Surrounding these activities are information and communication systems. These enable the organization’s people to capture and exchange the information needed to conduct, manage, and control its operations.

- Monitoring – The entire process must be monitored and modified as necessary. Thus, the system can react dynamically to changing conditions.

The following models show the relationships among these components:

COSO Cube shows the relationship between units, activity and objectives.

The Control Environment provides an atmosphere in which people conduct their activities and carry out their control responsibilities. It serves as the foundation for the other components. Within this environment, management assesses risks to the achievement of specified objectives. Control activities help ensure that management directives are carried out to address the risks. Meanwhile, relevant information is captured and communicated throughout the organization. The entire process is monitored and modified as conditions warrant.

Types of Controls

Many types of controls can help management direct their activities, such as:

- Preventive Controls are intended to deter inappropriate events from happening. These are the best types of controls, but they are typically the most expensive to implement.

- Detective Controls are actions that are taken to detect and correct undesirable events that have already occurred.

- Directive Controls are to trigger a desired behavior or event to occur.

Often, the best strategy is a combination and collection of all types of controls used together that enable an organization to achieve its goals and objectives.